ATED was introduced as part of a package of measures intended to deter the ownership of high value residential properties in structures that would allow the properties to be transferred or enjoyed without incurring a charge to stamp duty land tax (SDLT). The other element of the package is a 15% SDLT charge when the property is acquired, and this is easily identified and paid at that point. However, ATED can easily be neglected as it needs to be considered separately for each acquisition and then reconsidered on an annual basis, and that annual basis is prospective rather than retrospective.

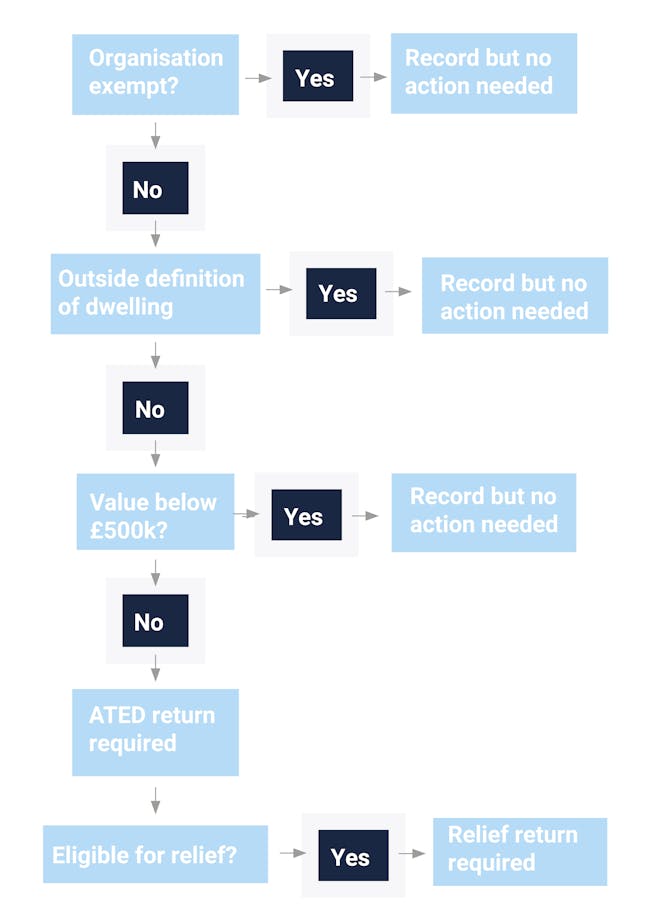

In addition, the combination of increasing property values and a drop in the minimum level at which the tax applies means that a property worth more than £500,000 constitutes a ‘high value’ property, even though this is the average value of a residential house in many areas.

Your organisation

The regime applies to non-UK resident and UK resident structures. A few organisations are exempt from the charge, such as charities, public and national bodies. Exemption does not need to be claimed.

Your property

Non-residential property is not within the charge. Instead, your organisation must have a beneficial interest in a residential property or ‘dwelling’. The nature of that interest is widely defined and covers not only freehold and leasehold interests, but also shares or interests in land and the right to receive rents. It is possible for there to be different interests in the same dwelling (such as the leasehold and the freehold) and each interest holder will need to consider their position.

Your organisation will need to be clear on the nature of not only your interest, but also that of any connected persons. This will determine what needs to be valued and, in some cases, value of different dwellings or interests may need to be amalgamated.

Only interests in those properties which are ‘dwellings’ are subject to ATED – a dwelling is a distinct unit of residential property, either in use already or suitable to be used as such and includes any associated land and buildings. It is possible to have one dwelling within the grounds of another (for example a main house and a cottage within an estate); more than one dwelling in a property (such as a block of flats or a terrace of houses), and multiple linked dwellings. However, some properties are specifically not classified as dwellings for these purposes and do not need to be reported – this includes hotels, guest houses, some forms of educational accommodation, hospitals, care homes and prisons.

Property values

Generally, property is valued at the later of its acquisition date or at a five-yearly valuation review date:

For the 2022/23 ATED year:

If you held the property on 1 April 2017, then its value at that date is used for valuation purposes, regardless of the price you originally paid for it.

If you acquired the property between 1 April 2017 and 31 March 2022, the value will be taken at the date of acquisition.

If you acquired the property on or after 1 April 2022, the value will be that at the date of acquisition.

For the 2023/24 ATED year:

If you held the property on 1 April 2022, then its value at that date is used for valuation purposes, regardless of the price you originally paid for it. This supersedes the April 2017 valuation.

If you acquired the property after 1 April 2022, the value will be taken at the date of acquisition.

It is good practice to establish the April 2022 value of any properties held at that date as evidence that either you are below the minimum level or to substantiate the banding of the property.

Valuation must be

for a specific price, rather than within a band. There is no obligation for you to have a formal

valuation prepared by an independent valuer.

You could gauge the value yourself using your knowledge of the property

and its surrounds. However, HMRC can

challenge that value so you should keep a record of the basis for your

calculation – if a challenge is successful, you may be subject to penalties as

well as additional ATED charges. If you

are in doubt and within 10% of a banding limit, you can ask HMRC for a

Pre-Return Banding Check (PRBC).

Revaluations are required if there is either a substantial acquisition or substantial disposal – broadly a transaction relating to an interest in that property worth more than £40,000.

Potential reliefs

Relief is available if the property is being used for qualifying purposes, which includes:

A property rental business

A dwelling open to the public

A property developer

A property trader

Occupation by certain employees

Working farmhouses

Conditions apply to these reliefs so you will need to check the rules carefully. For example, although a property rental business is a qualifying purpose, no day is relievable if the property is let to a non-qualifying individual such as connected person.

Relief must be claimed on a separate Relief Declaration Return and does not remove your responsibility to file an ATED return. However, If any relief reduces the ATED liability to nil, you can use a simplified return. The same deadlines apply for submitting claims for relief as for submitting the ATED returns.

ATED administration

The ATED year runs from 1 April to 31 March. Tax is due for that period if, on any day, your organisation is entitled to the interest in a dwelling that exceeds the £500,000 value. A separate return is required for each property.

An in-year return will be required if your organisation acquires a property or an existing property becomes a dwelling, so that an ATED charge will arise. The return needs to be filed within 30 days of the acquisition or within 90 days of a newly built property becoming available for use as a dwelling.

Returns and any tax payments are generally due by 30 April at the beginning of each ATED return period, so by 30 April 2022 for the ATED year to 31 March 2023.

Returns can be made online, but your organisation will need to register to do so. You can also appoint an agent to act on your behalf. These processes are separate from the usual tax and accounts authorisation.

HMRC can charge interest and penalties for late payment of tax, for not submitting a return or for submitting an incorrect return.

What tax is due?

Subject to reliefs, you are potentially subject to an ATED charge for each property. The amount of the charge depends on the valuation band within which your property falls. For the 2022/23 ATED year, the amount of tax chargeable is:

| Taxable value of the interest on the relevant day | Annual chargeable amount |

| £500,0001 to £1,000,000 | £3,800 |

| £1,000,001 to £2,000,000 | £7,700 |

| £2,000,001 to £5,000,000 | £26,050 |

| £5,000,001 to £10,000,000 | £60,090 |

| £10,000,001 to £20,000,000 | £122,250 |

| More than £20,000,000 | £244,750 |

Charges generally increase by inflation and new rates are announced each March. The tax is payable in full by 30 April at the beginning of each ATED return year.

If the ATED charge does not apply for the whole of the chargeable period, then a fraction is payable based on the number of days for which it does apply. This interim relief may be claimed before the end of the chargeable period if the charge does not apply because the property is subject to ATED relief, or your organisation has ceased to be chargeable, or the taxable value of the property has reduced (for example due to a part-disposal). Interim relief must be claimed in a return or in an amended return.

Similarly, you may need to make adjustment to the amount chargeable to ATED where the total due differs from the amount charged initially, perhaps because eligibility for a relief changes or you dispose of the property. If the adjusted amount is less than the original, you claim relief in a return or amended return by the end of the chargeable period following the one to which the claim relates. If the adjusted amount is greater, you must submit a further return and pay any additional tax due within 30 days of the end of the chargeable period.

Conclusion

The main focus on ATED tends to be in March/April each year when annual returns are required, and it is essential that your organisation has a robust method of making sure that you are compliant with the regime. However, ATED can also be increased or triggered during the year, so you also need to be satisfied that you have a process to confirm the ATED position in time to meet the reporting deadlines.

This article is intended to give a general introduction to ATED and, from time to time, we will produce news items concerning topical issues. We would always recommend you obtain specific advice on your organisation’s particular circumstances – if you would like our help, please do get in touch with your usual contact or use the link below.